It is no surprise that U.S. trade policy has dominated global news, and potential tariffs have introduced uncertainty into international trade. While the direct effects of tariffs on trade are widely understood, the anticipation of such measures has influenced commodity markets.

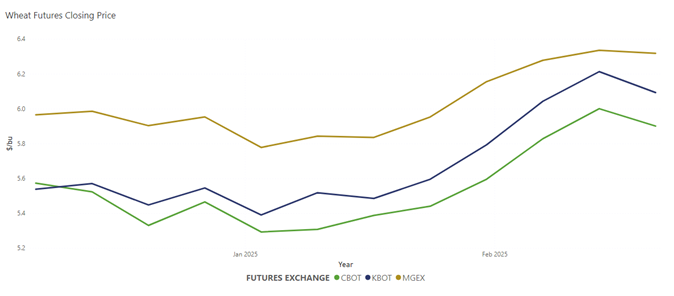

Concurrently, wheat markets experienced upward pressure, driven by a combination of factors including weather-related risks, dollar strength, and trade uncertainty. As a result, between January 1 and February 19, Kansas City Board of Trade (KBOT) wheat futures increased by 11%, Chicago Board of Trade (CBOT) by 8%, and Minneapolis Grain Exchange (MGEX) by 7%. Although prices have since retreated, we are sharing background on the factors that influenced the recent rally and highlight some of the lingering impacts.

Trade and Currency

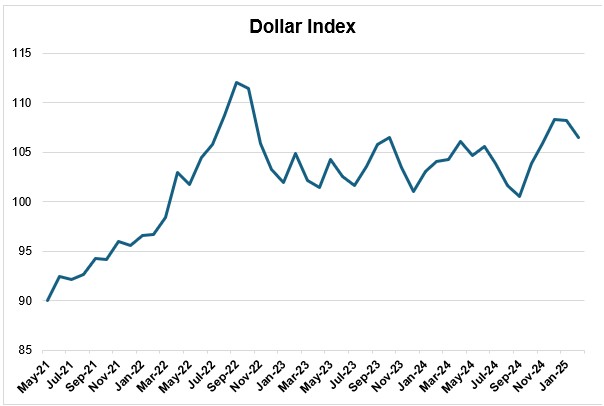

Since September, the U.S. Dollar Index, which measures the strength of the dollar against a basket of other global currencies, has risen by 6%, peaking at 109.9 on January 13. This represents the highest rate since October 2022, when the dollar strengthened significantly following a series of aggressive interest rate hikes by the U.S. Federal Reserve.

This strength is related to potentially higher inflation, economic uncertainty, and altered trade flows in response to changes in U.S. trade policy, which can prompt currency markets to “price in” added risk. Moreover, the dollar is often seen as a “safe haven currency” for its stability and value during periods of economic uncertainty. The increased demand for dollars during these times can further contribute to currency strength.

As customers are keenly aware, a strong dollar makes U.S. exports, including wheat, more expensive. A strong dollar also buoys futures prices as markets adjust to account for its impact.

Weather Risks

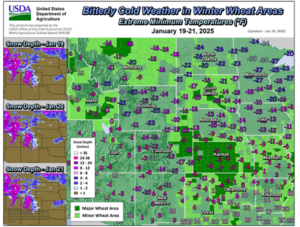

Weather also rises as a key price mover as wheat transitions into “weather market” season. The U.S. Southern Plains saw cold, dry conditions throughout January and early February, with temperatures 12°F to 15°F below average with only sparse snow cover. The combined impact of severe cold and lack of insulating snow cover raised winterkill risks for wheat. Likewise, Russia faced similar conditions, with frigid temperatures following a dry winter. Due to dryness, early 2025/26 Russian crop estimates have come in as low as 78.7 MMT.

The freezing weather in both the U.S. and Russia supported wheat markets. Temperatures have moderated and insulating snow helped alleviate some risk, but the impacts will remain unknown until spring.

A Look Ahead

As immediate winterkill risks subside, futures have begun to fall. Despite recent declines in prices, market volatility is expected to persist as the Northern Hemisphere crop begins to break dormancy and we enter the “weather market.” Furthermore, ongoing uncertainty related to trade will continue to support prices in the near term.

Looking ahead, markets await updated acreage estimates from the USDA Ag Outlook Forum, Prospective Plantings and the March WASDE, as well as further insights on the impacts of Russian export quota, that was effective February 15. U.S. Wheat Associates will continue to monitor world weather conditions, trade, and other market movers into the next phase of the 2025/26 wheat crop.

By USW Market Analyst Tyllor Ledford