Early Optimism Blooms for 2024 U.S. Winter Wheat Production

Drought in major U.S. wheat-growing regions over the past few years is well-documented. The persistent dry conditions acutely impacted U.S. wheat yield and increased abandonment, with 2023/24 production coming in 6% below the pre-drought five-year average. Now, entering the second half of the marketing year, the focus has shifted to the 2024 harvest and its […]

USW Analyst Shares Global Wheat Market Summary with Farmer Directors

U.S. Wheat Associates (USW) Market Analyst Tyllor Ledford compiles a comprehensive “World Wheat Supply and Demand” summary for three USW Board of Directors meetings each year. Using the USDA World Agricultural Supply and Demand Estimates (WASDE) report as her primary source, Ledford prepared the attached market summary for the USW Winter Board Meeting in Washington, […]

U.S. Wheat Export Basis Levels Support On-Going Competitiveness

During the summer of 2023, U.S. wheat export basis levels hovered near record lows as slow demand met seasonal weakness. Across almost all the U.S. wheat classes and export points, export basis levels hovered below average, signaling a unique pricing opportunity for U.S. wheat. Historical trends indicate that basis levels generally hit their lowest point […]

China’s Soft Red Winter Purchases: The Right Wheat at the Right Time

The purchase by China of 1.12 million metric tons (MMT) of U.S. soft red winter (SRW) wheat for delivery in 2023/24 between Dec. 4 and 8 is a significant and, in terms of its volume, somewhat unexpected factor in the current market. The buyers clearly took advantage of a price opportunity, yet there are other […]

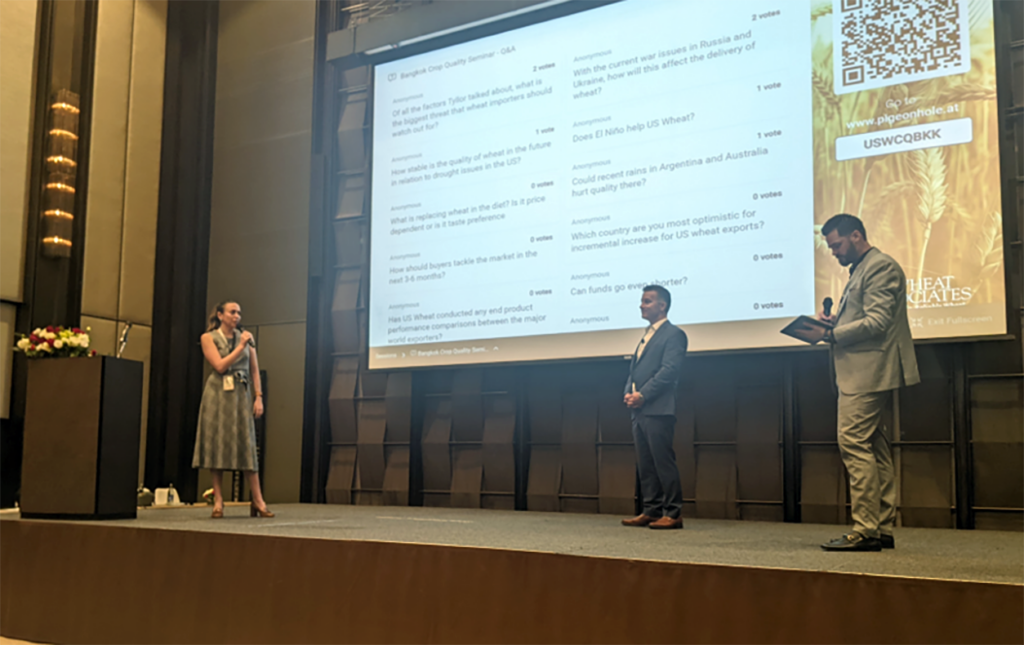

Market Analyst Shares Crop Quality Seminar Experience, Customer Feedback

Following is USW Market Analyst Tyllor Ledford’s report on her participation in the 2023 Crop Quality Seminars. She appears on the left in the photo above with Regional Vice President for South and Southeast Asia Joe Sowers and Assistant Regional Director Joe Bippert at the Crop Quality Seminar in Bangkok, Thailand. For many, the month […]

Investments in U.S. Supply Chain Infrastructure Benefit Wheat Importers

Over the last few weeks, we have explored all the major modes of the U.S. supply chain, evaluated recent trends, and highlighted how each type of transportation plays an integral role in the U.S. supply chain. Barging, rail, and oceangoing vessels work together to create the dependable supply chain importers of U.S. wheat expect. In […]

World Wheat Prices Hover at Lower Levels With Bullish Factors Lurking

Since the start of the year, world wheat prices have consistently trended lower, with Russian wheat maintaining its position as the world’s cheapest origin. With the Northern Hemisphere wheat harvest now complete, it brings about the question: have markets touched their seasonal lows, and in what direction will they go next? In this article, we […]

Rising Ocean Freight Rates Pushed by Uptick in Fuel Costs, Chinese Demand

In a series of articles on U.S. supply chain transportation, we have explored the importance of barging and rail on U.S. wheat exports and how they contribute to the reliability of the U.S. marketing system. Barging and rail account for 89% of all U.S. wheat export shipments. After traveling through the inland logistics system, on […]

Wheat Industry News

News and Information from Around the Wheat Industry Speaking of Wheat “Amidst the backdrop of diverse perspectives and conflicts of our times, farmers continue planting seeds of sustenance and resilience, stewarding the land for generations, and producing a safe and reliable food supply. The values of integrity, honesty, and care we see in agriculture offer […]

Most Exportable Supplies Moved by Rail with Significant Effect on Basis

As we continue a series of articles on U.S. supply chain logistics, rail is arguably the most important mode of transporting wheat for export. According to a recent USDA Modal Share Analysis Study, rail accounted for an average of 59% of inland transportation for wheat exports between 2016 and 2020, or an average annual total […]