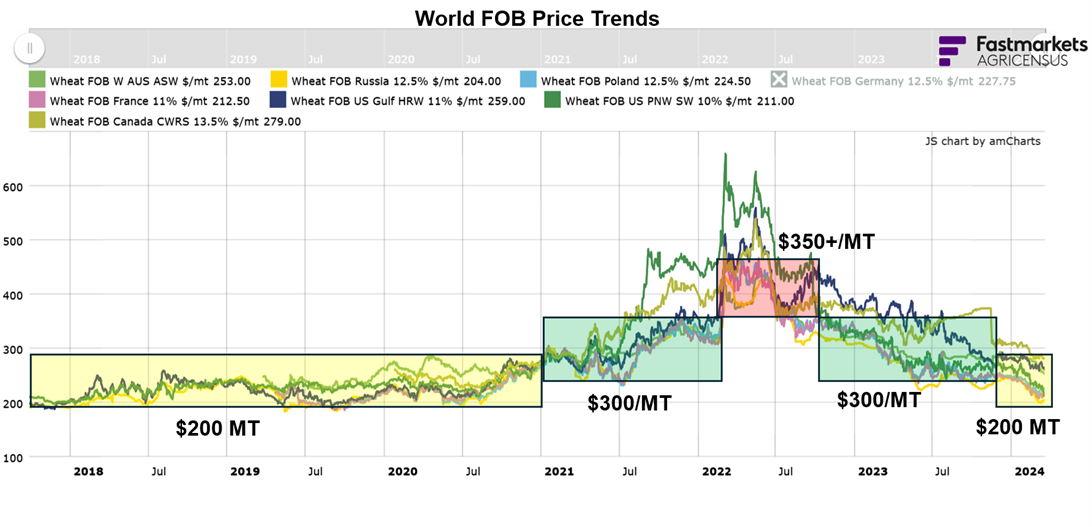

Over the last year, world wheat prices have trended steadily lower, continuing their fall from the highs hit in May of 2022 after Russia invaded Ukraine. Ample wheat stocks from Russia and record exports flowing from the Black Sea continue to weigh on global wheat prices.

The average world FOB price has decreased $32/MT from the start of 2024 and is nearly $255/MT less than the May 2022 high, according to AgriCensus price data. Although the war still rages in Ukraine, the war risk premium has eroded in the market, allowing prices to revert to pre-war trends. The following will outline the current price situation and highlight factors to watch as wheat markets align with long-term trends.

A Return to Pre-War Levels

Although there is a sharp contrast between the current downward trend in global wheat markets and the volatility observed over the last year, wheat prices have fallen more in line with long-term trends. Current world FOB prices hover between $200 and $300/MT on average, in line with price levels from 2018 to 2020. Although the spread between origins is still larger than pre-war averages, the spread has narrowed over the last year. According to AgriCensus and U.S. Wheat Associates Price Report data, in Jan. 2023, U.S. soft red winter (SRW) wheat sold for $347.96/MT FOB, while Russian wheat (12.5% on a dry moisture basis) was loaded at $308/MT FOB, a nearly $40/MT spread. Jumping ahead to March 21, 2024, U.S. SRW is quoted at $216.24/MT FOB, while Russian FOB indications sit at $204/MT, down to a $12/MT spread, similar to spreads seen throughout 2019 and 2020.

Factors to Watch

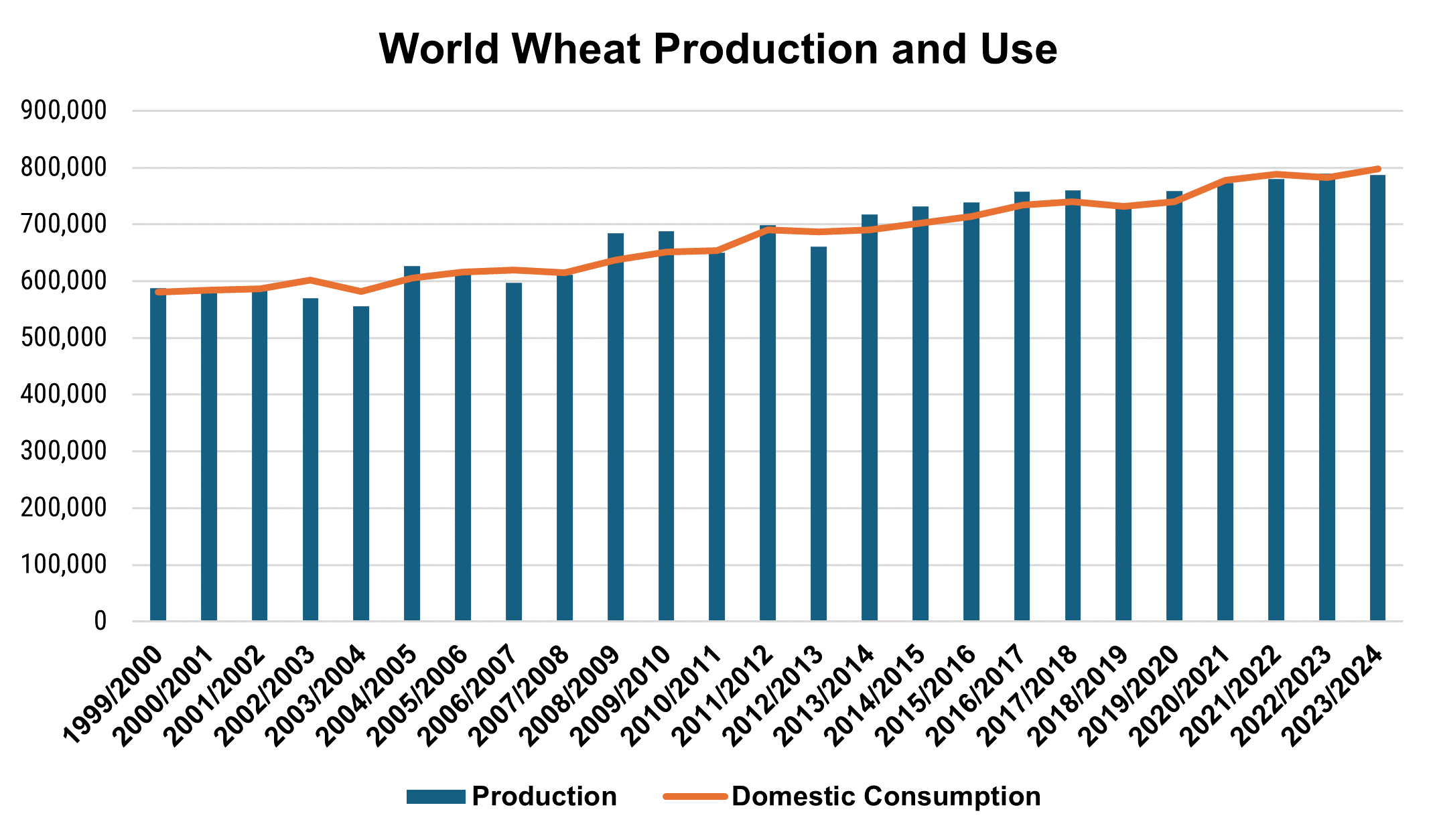

U.S. Wheat Associates (USW) is monitoring several factors at work in the global wheat market. Even before Russia’s invasion in Feb. 2022, global price levels were beginning to rise. Wheat use jumped 5% to a record 787 MMT in 2020/21, exceeding production by 14.0 MMT. The March World Agricultural Supply and Demand Estimates still put the 2023/24 global wheat consumption 11.0 MMT above production, further tightening stocks. Likewise, the stocks-to-use ratio, excluding China, is forecast to tighten to 20% in 2023/24, the lowest since 2007/08, while early estimates from the International Grains Council predict a decrease in global ending stocks to 57.0 MMT in 2024/25.

Looking ahead to marketing year 2024/25 and beyond, a continued decline in world-ending stocks and the tightening stock-to-use ratio may have a bullish influence on price trends. However, in the short term, global wheat markets remain well-supplied, and the ongoing flow of wheat from Russia, the Black Sea, and the EU weighs on prices.

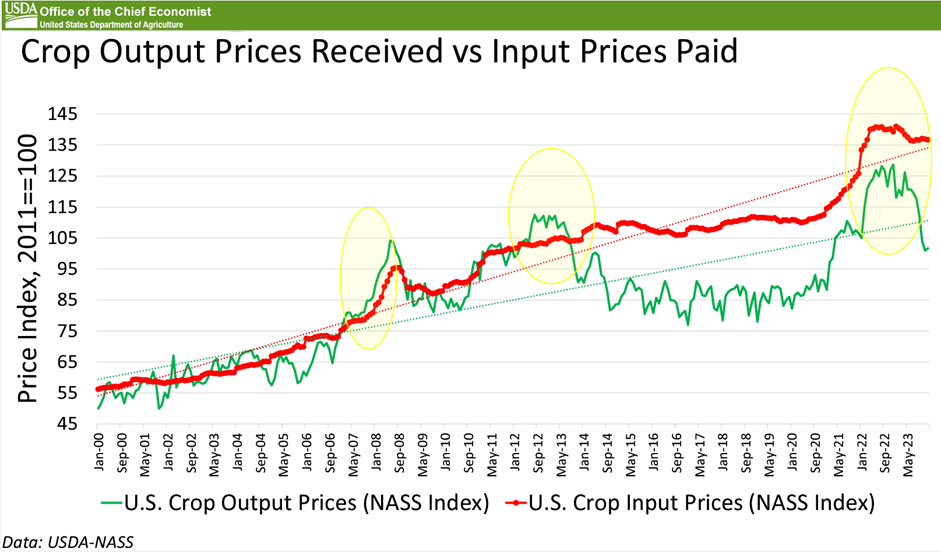

While decreasing wheat prices benefits importers, the current situation poses unique challenges for U.S. wheat farmers. According to Seth Meyer, USDA Chief Economist, input price trends lag as the output prices fall, resulting in tighter profit margins and reduced sector profitability for wheat and other row crops. Tighter margins put additional pressure on U.S. farmers, and long-term profitability can influence production trends and planting decisions. Nevertheless, U.S. farmers planted wheat before the war and will continue to produce a range of high-quality wheat classes as markets revert to pre-war norms, ensuring a reliable supply of wheat for the world’s importers.

By Tyllor Ledford, USW Market Analyst