U.S. Wheat Associates (USW) Market Analyst Tyllor Ledford compiles a comprehensive “World Wheat Supply and Demand” summary for three USW Board of Directors meetings each year. Using the USDA World Agricultural Supply and Demand Estimates (WASDE) report as her primary source, Ledford prepared the attached market summary for the USW Winter Board Meeting in Washington, D.C., Jan. 23 to 26, 2024.

Following is the start of Ledford’s report. Continue reading the entire report here.

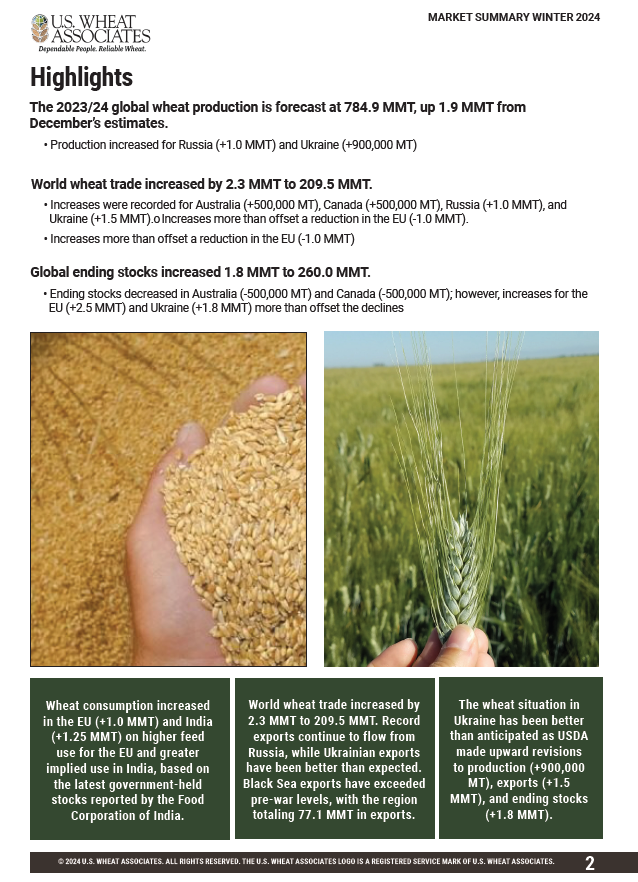

World Wheat Supply and Demand

Released on January 12, the World Agricultural Supply and Demand Estimates (WASDE) had a bearish impact on the market, as the estimates quantified the sustained record export flows from the Black Sea and increased ending stock levels. The 2023/24 global wheat production is forecast at 784.9 MMT, up 1.9 MMT from December’s estimates. Meanwhile, world wheat demand remains at a record high of 796.4 MMT, outpacing world wheat production by 11.5 MMT

Although demand surpassed supplies, the January WASDE increased world ending stocks by 1.8 MMT. The current estimate of 260.0 MMT is a 4% decrease from the year prior and the lowest level since 2015/16. In major exporting countries, wheat stocks sit at 58.7 MMT, an improvement from previous estimates but still below 60.4 MMT the year prior. Increased ending stocks in the EU and Ukraine helped support the recent increases. World wheat trade is expected to reach 209.5 MMT, down from 220.2 MMT in 2022/23.

Domestically, the January WASDE made few significant changes, while the Winter Wheat Seedings Report overshadowed the WASDE’s impacts. U.S. ending stocks came in 300,000 MT lower, though USDA foresees ending stocks at 17.6 MMT, a 14% increase year over year and the first increase since 2015/16. That estimate helps loosen the U.S. wheat balance sheet and relieve underlying price pressure, though ending stocks still sit 13.9 MMT below the recent highs hit in 2016/17.