Spring’s arrival in the Northern Hemisphere typically brings a period of weather-related market volatility, a pattern that has held true this crop year. However, ongoing uncertainty from dynamic policy changes is shaking the usual seasonal in the U.S. wheat trade outlook.

Weather Market Whiplash

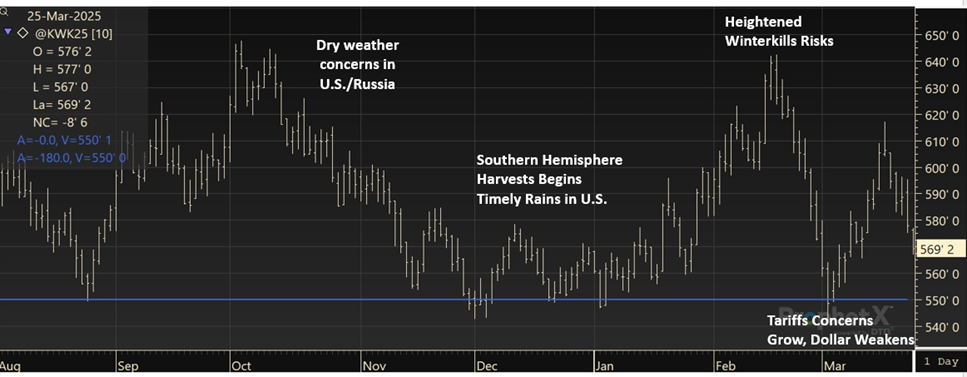

In February, concerns over cold and dry conditions in the Black Sea and the U.S. propelled futures markets to their highest levels since October 2024. However, as fears of winterkill eased with insulating snowfall across the region, futures prices experienced a sharp decline. Between February 18 and March 3, CBOT wheat futures plummeted by 70 cents, KBOT by 74 cents, and MGEX by 68 cents.

Markets have since recovered, finding support at established psychological price floors. Markets will continue monitoring the weather in the U.S. Southern Plains, especially after unseasonably warm temperatures and severe windstorms intensified existing dryness. Additionally, attention will be given to conditions in the Black Sea region as drought continues, and to crop development within the European Union, where heavy moisture has emerged as a persistent issue following last year’s unusually wet growing season that adversely affected yields.

Tariffs and Trade Exert a Bearish Influence

The implementation of new tariffs has had a chilling effect on trade prospects, the full extent of which remains to be seen. This policy-induced uncertainty, coupled with the inherent market volatility, creates a complex and challenging landscape for U.S. wheat. The situation changes daily, but U.S. Wheat Associates continues to monitor the tariff landscape and evaluate its impacts on trade as information becomes available.

The U.S. Trade Representative’s (USTR) proposed Section 301 remedies against China’s maritime and shipbuilding sectors, including substantial port fees and mandated U.S.-vessel usage, have further dampened the trade outlook. U.S. Wheat Associates (USW), along with exporters, customers, farmers, and other industry stakeholders, has voiced concerns about the negative impact on U.S. wheat exports and agricultural competitiveness. While no measures have been implemented, the proposed actions are already negatively impacting the U.S. export outlook in the near term.

The USDA World Agricultural Supply and Demand Estimates (WASDE) only considers trade policies that are in effect at the time of publication. Further, unless a formal end date is specified, the report also assumes these policies remain in place. Nevertheless, the March WASDE also added to the bearish sentiment. Ending stocks in major exporting countries increased by 6% from last month to 57.2 MMT on production increases for Australia and Argentina and declines for the U.S., Russia, and the European Union. Overall, the combined impact of decreased exports and higher ending stocks weighs wheat markets as supplies remain adequate.

Positive Highlights

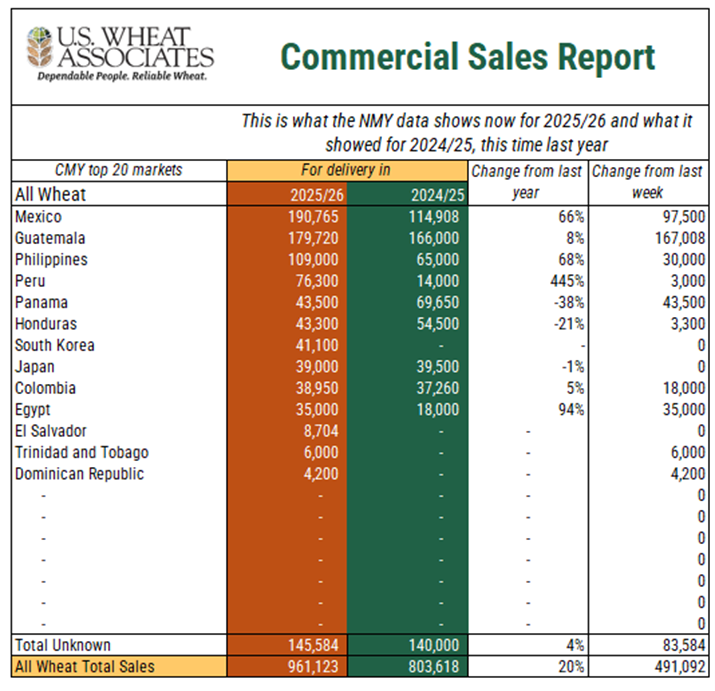

Despite these headwinds, a slight weakening of the U.S. dollar offers a glimmer of hope, potentially enhancing the competitiveness of U.S. grains in the global market. Additionally, recent bearish trends have aligned U.S. wheat classes more closely with global origins. The spread between U.S. HRW and the cheapest global origins are nearing their most consistently narrow margin to date. Boosted by the increased competitiveness, marketing year 2024/25 wheat sales currently sit at 20.8 MMT, a 13% increase from last year, putting them at 92% of USDA’s projected exports with just 10 weeks left in the marketing year. For the marketing year 2025/26, sales hover around 961,000 MT, a 20% increase from this time last year as many exporters swap from old crop to new crop delivery periods.

Looking ahead, wheat markets will remain sensitive to weather developments and policy changes, particularly in the months leading up to the Northern Hemisphere harvest. Clarity on tariffs and the trade outlook is expected on April 2, while upcoming rains in the Black Sea and Southern Plains may influence crop conditions. For important new crop updates and market information, market participants should monitor the USDA Prospective Plantings Report, due on March 28, the USW Harvest Reports, USW Price Report, and the May 2025 WASDE.

By USW Market Analyst Tyllor Ledford