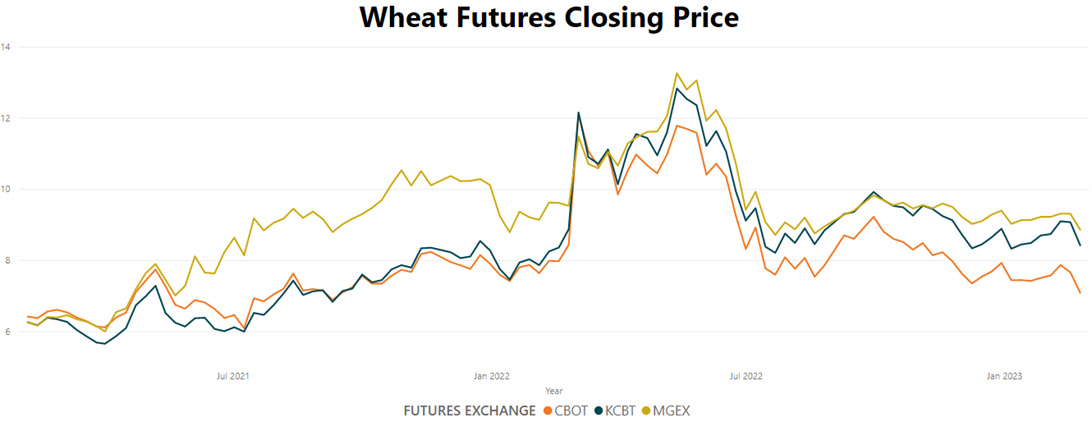

Since Russia’s unprovoked invasion of Ukraine sent them soaring one year ago, global and U.S. wheat prices have decreased significantly. Continued Black Sea Grain Corridor exports and improved production outlook in major exporters such as Russia and Australia have helped relieve the market of some supply pressure. Bulk ocean freight rates have also broken in favor of wheat and other grain importers.

Even more relief for buyers arrived with the USDA Grains and Oilseed Outlook released on Feb. 23 that projected an 8% increase in all U.S. wheat planted area. On Feb. 24, wheat futures fell as much as 30 cents overnight in response to that report.

In a classic supply and demand equation, tight global wheat stocks and the uncertainty of the Black Sea pushed prices higher and provided an economic incentive to plant more wheat and futures prices reacted to the news.

Historical Perspective

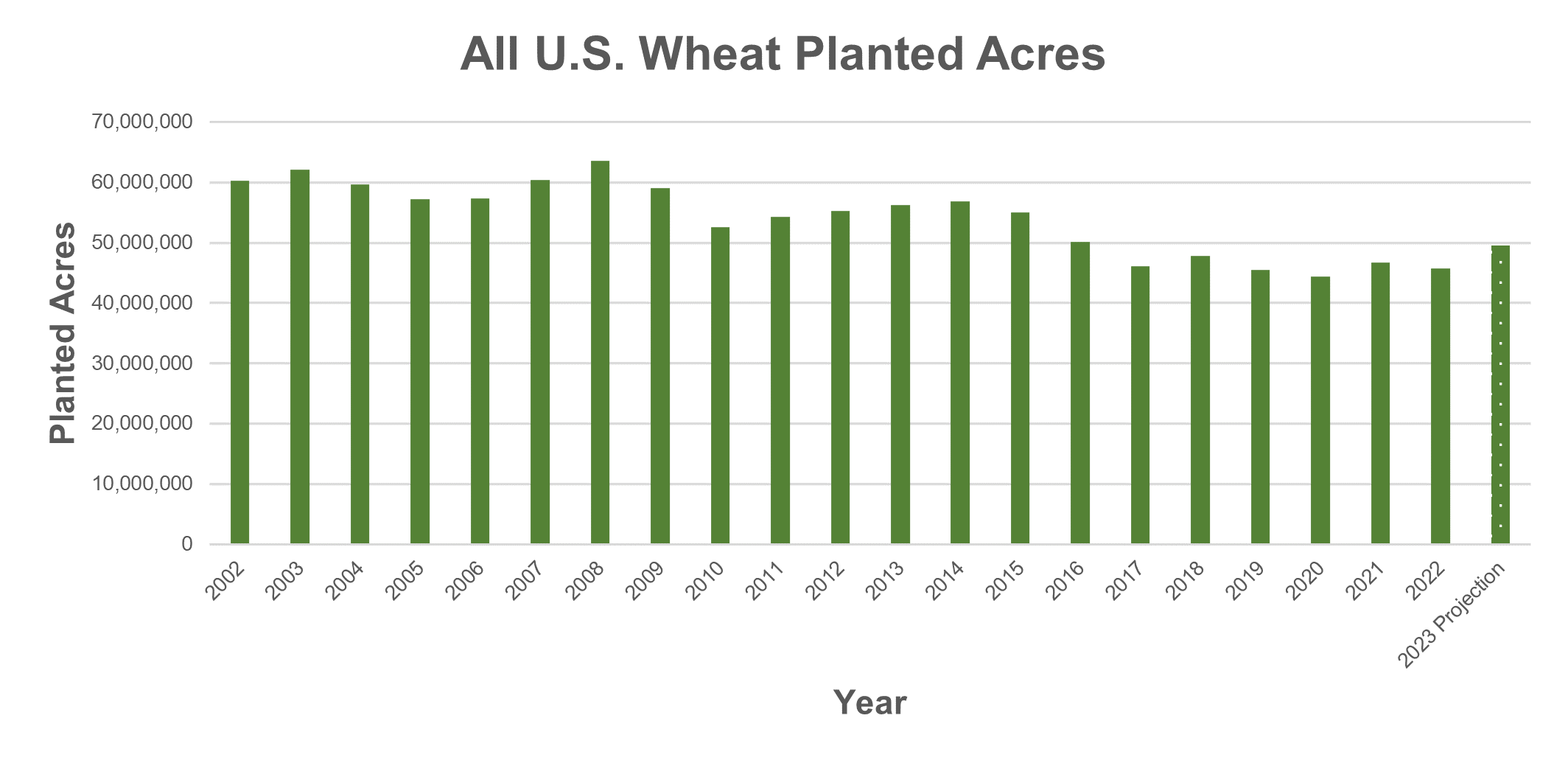

Over the last two decades, competition for wheat acres has increased as profit margins have shifted to favor other crops such as corn and soybeans. Meanwhile, as market volatility persists, farmers increasingly utilize diversified crop rotations to mitigate price and input risk. The combined impact has resulted in a slow erosion of U.S. wheat annual planted area, with the most recent five-year average coming in at 46.0 million acres (18.6 million hectares), down 24% from the 2002.

In addition to supply pressures at home, enhanced production in competing exporters has highlighted the increasingly tight U.S. balance sheet. Production in Russia has increased 76% over the last decade, while Argentine production, increased 138% from 2012/13 to 2021/22, (excluding the historic drought impacting the 2022/23 crop).

Wheat planted area erosion and increased global competition, coupled with drought-inflicted production shortfalls in the U.S. over the last three marketing years have created a tight balance sheet both domestically and on a global scale, underpinning wheat prices.

A Break in the Trend

Breaking from the historical trend, in January 2023, the USDA Winter Wheat and Canola Seedings report projected the 2023 winter wheat seeded area at 37.0 million acres (14.9 million hectares), up 11% from 2022 and 14% above the five-year average. The Hard Red Winter wheat (HRW) area was up 10% to 25.3 million acres (10.2 million hectares), while white winter wheat is up by 3% to 3.73 million acres (1.5 million acres). Soft Red Winter wheat (SRW) experienced the most significant planting increase, jumping 20% from 2022/23 to 7.9 million acres (3.2 million hectares)

Further echoing the sentiment for increased planted area, the recent USDA Grains and Oilseed Outlook projected an 8% increase in all wheat planted area to 49.5 million acres (20.0 million hectares), driven primarily by the jump in winter wheat acres. The estimate is the highest since 2016 and 8% above the five-year average.

Looking Ahead

As producers begin their spring wheat sowing campaigns, Jim Peterson, Policy and Marketing Director at the North Dakota Wheat Commission, notes that though there is room for increased planting, many farmers minimized price risk by locking in their crop rotations and inputs for the season early, which tempers major acre shifts. He also added that spring wheat planted area increases this year would be in part a rebound after last year’s wet spring prevented many acres from being planted.

More clarity will come on March 31, when USDA publishes its annual Prospective Plantings Report outlining the initial spring wheat area and updating winter wheat area estimates. Likewise, the May 2023 World Agricultural Supply and Demand Estimates will provide the government’s first insight into the 2023/24 marketing year.

The incentive to plant wheat remains strong, but planted acres do not necessarily equate to production, especially as drought conditions persist in the southern plains. As always, the weather will play a crucial role in crop production as spring planting begins and the winter wheat crop emerges from dormancy.

By USW Market Analyst Tyllor Ledford