With a significant decline in U.S. wheat production, the September 30, 2022, the USDA/NASS Small Grains Summary report took many wheat traders and analysts by surprise. The report estimated total production at 44.91 million metric tons (MMT) 1.65 billion bushels of total U.S. wheat production, down 3.62 MMT from August estimates.

The quarterly report is the culminating outlook for the U.S. wheat crop and follows the Grain Stocks report in January, the Prospective Plantings report released in March, and the Acreage Report released in June.

An article in Farm Futures, noted that all the pre-report trader estimates missed the mark except for white wheat production. Wheat futures rallied after USDA released the Small Grains Summary. December 2022 Chicago soft red winter futures closed 3% higher on the tighter outlook. Kansas City and Minneapolis exchanges were also higher. Reflecting the now apparently standard volatility, futures prices then retreated as speculators adjusted their market positions at the start of the new month.

Behind the Production Drop

U.S. wheat farmers faced many obstacles this year. Hard red winter (HRW) farmers experienced prolonged hot and dry conditions in the lower Plains states, especially Kansas, Oklahoma, the Texas Panhandle, and Colorado. In the upper Plains states, hard red spring (HRS) farmers faced heavy rain and cool temperatures early in the planting season, causing planting delays and ultimately lowering the amount of spring wheat area planted this year, offset a bit by an increase in harvested area compared to the 2021 drought year.

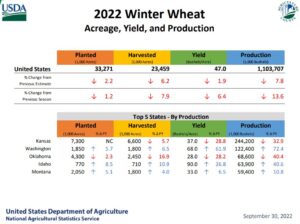

The Small Grain Summary showed an improved yield when combining all wheat classes. The “All Wheat Classes” yield was up 5% from 2021 at 46.5 bushels per acre (bu/acre). The improved yield was boosted by a dramatic recovery in spring wheat which the report recorded at 46.2 bu/acre compared to 32.6 bu/acre in 2021, a 42% improvement in yield. However, winter wheat yield was down 6% compared to 2021 at 47 bu/acre. Durum wheat also saw a significant improvement in yield year-over-year at 40.5 bu/acre up 64% compared to last year.

WASDE Reflects Changes

The USDA applied the revised production data from its Small Grains Summary in its October World Agricultural Supply and Demand Estimates (WASDE) on October 12. While 2022 production was lowered 3.62 MMT, beginning stocks were raised. Looking ahead, 2022 ending stocks were lowered, led by a 900,000 MT reduction in SRW stocks. The ending stocks estimate, pegged at 15.68 MMT, is down nearly 14% from last year and, if realized, would be the lowest since 2007/08. Exports were trimmed 1.09 MMT to 21.09 MMT, if realized this will be the lowest export total in over 50 years (noting that U.S. exports were 21.20 MMT in marketing year 2015/16).

New Information, Different Result

In keeping with the volatile pattern, despite USDA’s latest estimate reducing total U.S. and world wheat production, futures did not rally as they did after the Small Grain Summary. Instead, the Chicago December SRW contract was down 18 cents. Kansas City HRW was down 20 cents, and the Minneapolis HRS contract was down 18 cents. Including supply changes, this market is loaded with uncertainty, including the on-going conflict in Ukraine, the high value of the U.S. dollar relative to other currencies, and news of challenging weather conditions here in the United States and other wheat exporting countries. As always, your local U.S. Wheat Associates (USW) representatives are ready to help the world’s wheat buyers navigate these challenging conditions.

By USW Market Analyst Michael Anderson