In a series of articles on U.S. supply chain transportation, we have explored the importance of barging and rail on U.S. wheat exports and how they contribute to the reliability of the U.S. marketing system. Barging and rail account for 89% of all U.S. wheat export shipments.

After traveling through the inland logistics system, on average, 90% of all U.S. wheat is exported via maritime transportation routes. Ocean freight is pivotal in wheat exports as the primary mode of transporting U.S. wheat to importers worldwide. With the significance of bulk ocean freight in mind, today’s article will evaluate recent trends in maritime transportation as rates begin to rise after an extended period of stagnant prices.

Fundamental Shifts

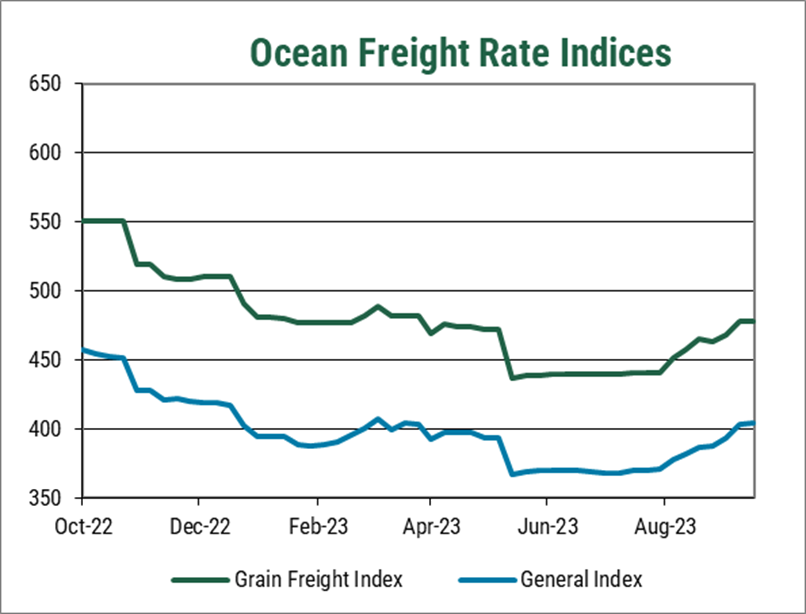

Throughout the fall of 2022, ocean rates steadily decreased, touching COVID-era lows in February 2023, driven down by low demand, an increasing supply of vessels, and normalized oil prices. After a brief uptick in March and April, freight rates and indices remained surprisingly stable until recently.

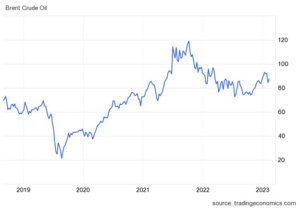

Oil prices are back on the rise after a steady decline throughout much of 2022 and the initial months of 2023. In April, major oil producers in OPEC and allied countries (OPEC+) decided to decrease oil production by 3.6 million barrels per day (3.7% of global demand). The OPEC+ alliance cited weak demand and “interferences” in the market (Western sanctions on Russian oil production) as the primary reasons for the shift. With rising oil prices, vessel owners are paying more for diesel fuel and pass on the extra cost to their bulk commodity customers via higher rates.

En Route to China

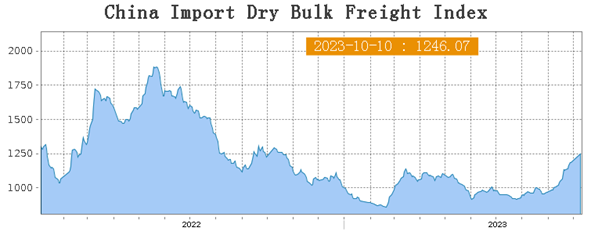

Moreover, China’s increasing freight demand is adding cost. In our last freight update, we highlighted China as one of the primary ocean freight rate drivers as the world’s leading importer of dry bulk commodities, specifically coal and iron ore. In 2022, China’s GDP growth slowed to 2.8% compared to 8.1% in 2021; as a result, manufacturing activity and demand for iron ore decreased, helping freight rates come down.

Since then, there has been a resurgence of Chinese economic activity and the possible infusion of 1 trillion yuan ($137 billion) in infrastructure projects and lower interest rates to boost the economy. Likewise, Chinese demand for agricultural commodities is on the rise. Recently, for example, China purchased more than 200,000 metric tons of U.S. soft red winter (SRW), the largest single purchase since 2019.

Issues To Watch

Despite recent positive signs for the Chinese economy, major property developer China Evergrande Group still faces repercussions of Chapter 15 bankruptcy, casting a shadow of doubt over Chinese economic recovery. At the same time, economists are unsure if recent gains will hold or if a stimulus would be sufficient to support the economy long term. Economic recovery in China, or lack thereof, will continue to drive dry bulk ocean freight trends in the near future.

Another ocean freight concern is the effect of low water levels on the Panama Canal. The Panama Canal serves 5% of world trade, and severe drought continues to impact trade flows. Only up to 32 ships are currently authorized to transit daily, down from 36 ships in normal conditions. Maximum vessel draft has decreased to 44 feet, down from 50 feet. Water levels at Gatun Lake, the primary water source for the canal, were at 24.2 meters (79.7 feet) in mid-September, down from 26.6 meters. It will be important to observe how the emerging El Niño weather pattern may affect water levels and, thus, transportation through the canal.

Integral Part of the System

As the last leg of the U.S. supply chain, ocean freight plays a significant role in transporting U.S. wheat to destinations worldwide. Monitoring trends in ocean freight is critical to understanding the cost and potential price risks for importers. Changes in ocean freight rates can greatly impact the landed cost of U.S. wheat for importers, so it is critical to distinguish what factors influence the price of U.S. wheat at every point in the supply chain, from inland logistics to the ocean vessel.

This article is part of a series outlining the transportation logistics for U.S. wheat, highlighting barge freight, the railroads, infrastructure investments, and maritime transportation trends.

By USW Market Analyst Tyllor Ledford