Across the Northern Hemisphere, wheat price and crop development are dominating market discussion. Soon, the first harvests of the 2024/25 crop year will provide more concrete information on supply availability and quality. Until then, weather conditions will play a crucial role in global grain markets as winter wheat enters late growth stages and spring wheat planting progresses.

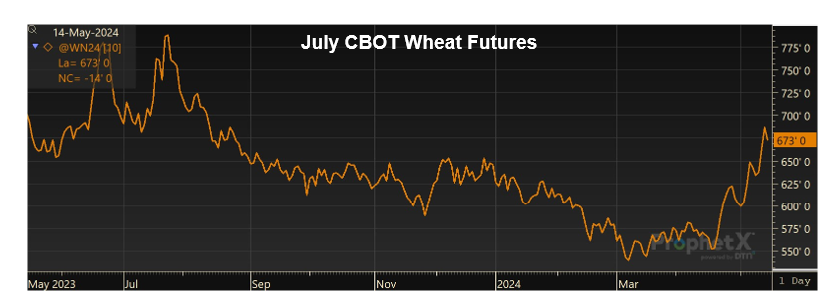

Although world wheat prices were trending steadily lower over the last year, shifting weather patterns have prompted a recent reversal. Since April 18, 2024, the July Chicago Board of Trade (CBOT) wheat futures contract has surged from $5.53 per bushel to $6.87 per bushel as of May 13, reaching its highest level since August 2023 (ProphetX chart image at the top of this page). Following is a look at recent market-moving weather developments and factors to watch as the 2024 harvest approaches.

Weather Swings Bring Attention to Russia

In the past month, varied weather conditions have raised concerns about the Russian wheat production outlook. Recent reports from Sovecon indicated that from mid-March to mid-April, moisture levels in southern Russia were 60% to 80% of normal and minimum temperatures were 2°to 4°C above average. Meanwhile from May 3 to 5, central and southern Russian crop growing areas suffered from severe frosts, potentially affecting the development of wheat, sugar beets, and other crops. Media sources reported air temperatures as low as -4.6 °C (23.7 °F) and soil temperatures near -5 °C (23 °F).

The combined impact of dryness and severe frosts prompted IKAR analysts to reduce their production estimates by 5.0 MMT to 86.0 MMT. Similarly, the May USDA World Agricultural Supply and Demand Estimates (WADE) predicted a 3.5 MMT drop for 2024/25 Russian output year over year. Throughout 2023 and early 2024 the large supplies of Russian wheat flooded the world market and depressed prices, highlighting the sizable influence Russia projects on global grain markets. Therefore, lower yield potential in Russia would have a significantly bullish impact on global prices.

Variable U.S. Conditions

On the domestic front, the overall outlook for the U.S. Southern Plains remain more optimistic as moisture levels and drought conditions improve. However, over the last few weeks, dry and variable conditions have raised concerns regarding 2024 production prospects. In Kansas, the largest HRW producing state, crop conditions have deteriorated rapidly, going from 57 percent good to excellent on February 25 to only 31 percent good to excellent by May 12. Likewise, conditions have worsened in Colorado, Oklahoma, and Texas due to windy and dry weather.

The persistent lack of moisture in parts of the Southern Plains may keep wheat prices elevated, but nevertheless, improving conditions in other areas and the potential for timely rains in drought afflicted regions could offset the impact. Overall, U.S. conditions still remain much improved from 2023, with 50% of all winter wheat rated good to excellent.

Results of the Wheat Quality Council’s Hard Winter Wheat tour May 14 to 16 will have their own, if brief, impact on futures prices.

Expect Increased Volatility

Until the crop reaches maturity and harvest begins in the Northern Hemisphere, weather will heavily influence futures markets. In the short term, prices will stay volatile in response to rapidly changing conditions and news. For up-to-date information regarding the current crop conditions and harvest outlook, look for the weekly USDA Crop Progress Report and the U.S. Wheat Associates Harvest Report. Also, watch the next “Wheat Letter” for discussion on the newest changes to the May WASDE and the first glimpse of what the 2024/25 marketing year will bring.

By USW Market Analyst Tyllor Ledford