In a market-moving report in February, USDA cut its 2021/22 global wheat production estimate by more than 2 million metric tons (MMT) from its January estimate. USDA also increased its world wheat consumption estimate.

What is behind this change so late in the marketing year?

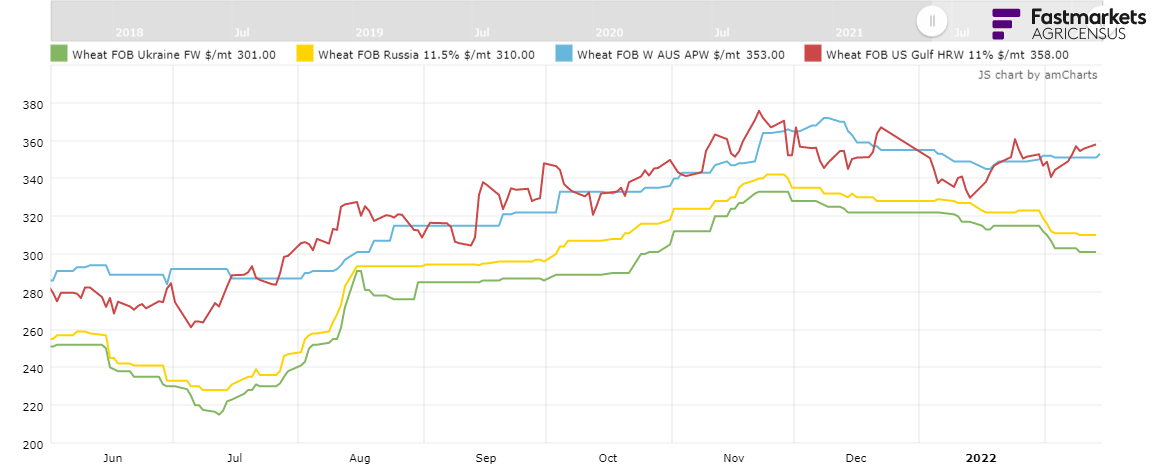

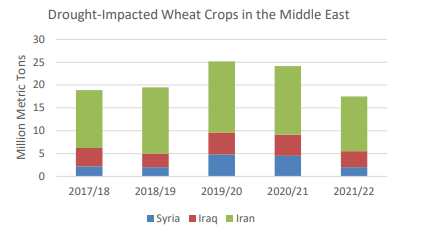

This year, high wheat prices remain a fixture as drought in major exporting countries cut trade supplies. However, coming into better focus is the hard-hitting drought in Middle Eastern countries that usually grow more wheat for domestic use.

Supply Restrained

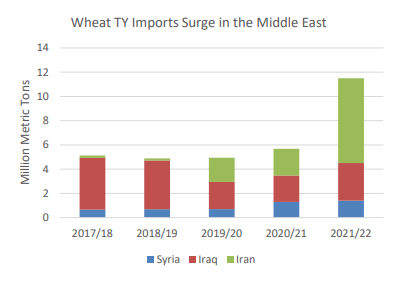

Iran, Syria, Iraq, Turkey, and Egypt have all seen crop reductions during the 2021/22 growing season, contributing to lower global wheat production. That suggests higher wheat import volumes will be needed to meet domestic demand. This is significant because, taken as a whole, the region is expected to import 35.5 MMT of wheat in 2021/22. That is 17% of USDA’s global import forecast of 204.8 MMT. In 2020/21, these five countries imported 25.9 MMT or 13% of the global wheat trade.

USDA’s Foreign Agricultural Service (FAS) report on Iran estimates wheat production to be down 3 MMT to 12 MMT total. Syrian wheat production is estimated at 2 MMT, and in Iraq, production is estimated at 3.5 MMT. Much of the production shortfall is being made up by imports from Russia, which enjoys a transportation advantage, FAS reported.

A look into the situation in these countries is helpful.

Iran

In October 2021, Reuters reported that Iran, which has imported around 1.0 MMT of wheat annually over the last five years, would need to import 8 MMT in 2021/22 to ensure a steady bread supply. The Foreign Agricultural Service forecast wheat imports at 7 MMT this year, up nearly 5 MMT compared to other years. Iran suffered its worst drought in half a century during the 2021 growing season, cutting the wheat crop by 30%, said industry sources.

Syria

In Syria, the “Year of Wheat” campaign has been challenged by low rainfall, leaving an import gap of 1.5 MMT. The United Nations (UN) Food and Agriculture Organization (FAO) said that Syria would need to import at least 1.5 MMT of wheat. The organization said the government’s target of 1.2 MMT of local wheat, purchased through forced sales of wheat from Syrian farmers to the government, “looked unrealistic.”

Iraq

Iraq’s state-grain buyer said it procured around 3.36 MMT of local wheat in 2021, down from 5.02 MMT in 2020. The Grain Board said in December it plans to import 2 MMT of wheat in 2022. Unlike the other countries discussed here, Iraq is less price-sensitive and buys high-quality wheat from U.S., Australian and Canadian origins. When Iraq’s Ministry of trade was actively tendering for wheat between 2017 and 2019, more than half its imports came from the United States. Before this year, two exceptionally large Iraqi wheat crops have met domestic demand.

Turkey

This month, the USDA/FAS agricultural attaché in Turkey reduced the estimate for wheat imports in 2021/22 by 5 MMT to 10.8 MMT. Even so, the revised estimate is 33% higher than imports from previous marketing years. The FAS office also said wheat production in 2021/22 had fallen 2 MMT to 16.25 MMT. The Attaché’s report is lower than the recent WASDE report, which put Turkey’s wheat imports at 11 MMT. The Turkish Statistic Institute showed that wheat imports during the first six months of the 2021/22 trade year (June-November 2021) grew by 20% year-on-year.

Egypt

Egypt is the largest importer of wheat in the world. It produces less than half the wheat it consumes annually. According to the Egyptian Supply Minister, the government is working hard to diversify its suppliers. The recent tension between Russia and Ukraine could disrupt 80% of Egypt’s grain flow. Despite an increased harvest forecast of 9 MMT for domestic wheat, 100,000 MT more than 2020/21, domestic consumption is expected to increase 400,000 MT. Egypt’s imports are expected to increase 7% compared to the 5-year average.

Drought, Supply and Prices

Global wheat production challenges fueled by drought have certainly driven this market in the past. And this month, USDA summarized its report this way: “the global wheat outlook for 2021/22 is for lower supplies, higher consumption, increased trade, and reduced ending stocks.”

The price incentive for farmers to produce more wheat for 2022/23 is real. The world will be watching to see if Mother Nature supports that effort.

By Michael Anderson, USW Market Analyst