This was supposed to be the year dry bulk freight vessel owners turned a profit, Jay O’Neil, a commodities consultant and author of a weekly transportation report recently commented. And U.S. Wheat Associates (USW) shared similar thoughts early in 2021. Instead, S&P Global Market Intelligence noted recently that freight rates for dry bulkers have fallen over the past three months after rates peaked earlier than expected in the second quarter of 2022.

As rates recently climbed, however, O’Neil said the freight market may have finally found its bottom.

Bearish Factors

Since early 2020, shipping has faced uncertainties: labor shortages, various COVID restrictions made worse by each country applying different restrictions, port congestion, and supply chain breakdowns have all competed to make shipping tough. The challenges to shipping logistics have abated. As a result, the number of available vessels floating in the dry bulk freight market has increased.

As China Goes…

China plays such a dominating role in the dry bulk shipping market that analyzing economic activity there can predict the dry bulk fleet’s prospects. China’s economic growth slowed under the government’s zero-COVID policy. The global iron ore trade, one aspect that drives the dry bulk fleet, was down 6% last month compared to a year ago. An analyst with S&P Global Market Intelligence said “slower than expected economic growth” could exist through the second half of 2023. O’Neil covered bearish factors for the dry bulk freight market for USW’s 2021 Crop Quality report.

Russian Coal

Putin’s war in Ukraine has also rerouted some cargo flows and driven up demand for coal, another commodity that absorbs dry bulk shipping capacity. Sanctions on Russian gas supplies have quickly reversed European Union plans to close many coal-fired plants. While the E.U. looks to the United States for coal imports, India and China are taking advantage of cheap Russian coal and changing demand for different bulker size categories.

Another key component that helped bring down dry bulk shipping rates is the easing of port congestion.

“Inefficiencies of last year do not apply to the current market anymore and the supply-demand equation is more straightforward,” said one ship owner. AXS said a primary driver behind the lower rates is the drop in ton-miles.

Overall, Breakwave Advisors, a shipping publication, agreed saying, “Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades.”

This was all good news for dry bulk freight customers, including the world’s wheat buyers.

Turning Tides

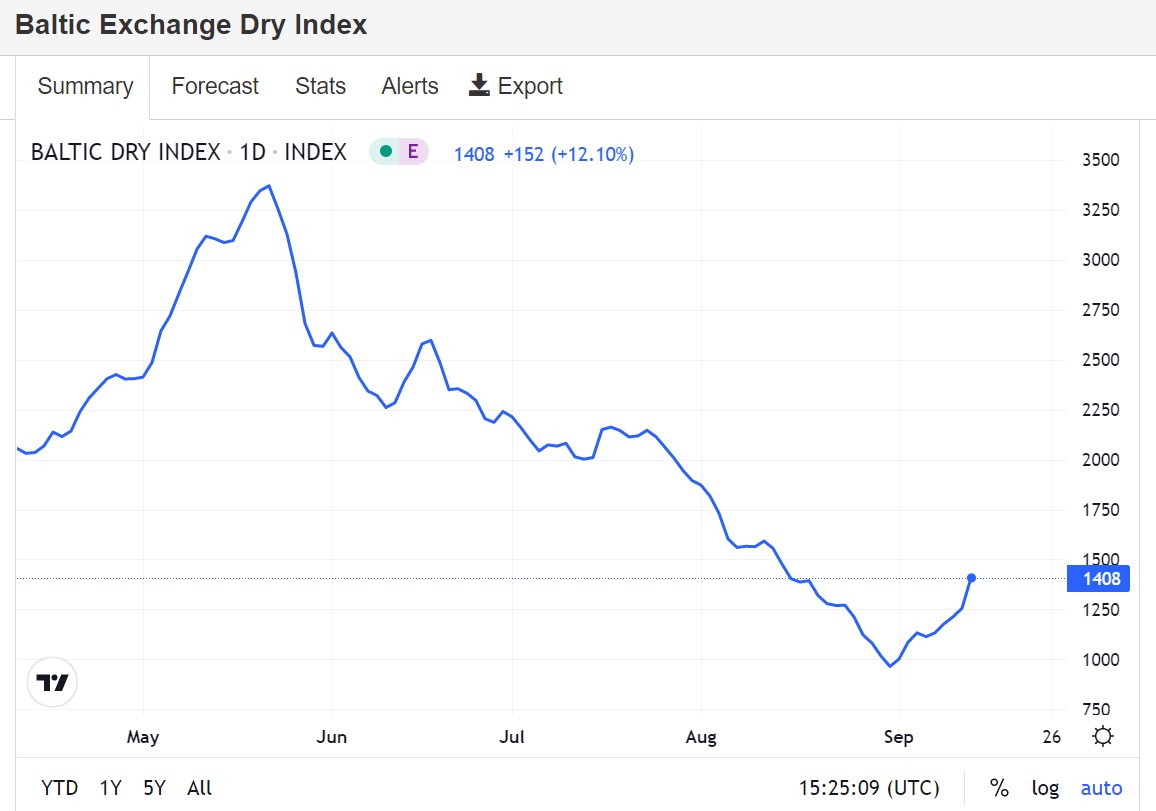

Yet signs of rate recovery are evident. The Baltic Index on September 9 notched its largest weekly increase in 8 years, according to Reuters data. The index was up 12% to 1,213. On September 12, the Baltic Index marked its fourth consecutive session of gain. AgriCensus, in a story published on August 31, noted that the purchasing managers’ index (PMI) rose to 49.4 in August, up 0.4 compared to July. But still, the index remained below the 50-point mark which separates contraction from growth.

Despite the current strengthening in the shipping index, generally bearish factors affecting dry bulk freight rates such as China’s economic situation remain. Those that follow the market closely say that rebound may simply be a market correction. For now, it seems like vessel owners may have to wait longer before turning that profit that many predicted not long ago.

By Michael Anderson, USW Market Analyst