A Deep Dive into Ocean Freight Market Factors

The recent run-up in ocean market freight rates is causing heartburn for the world’s grain importers. Vessel rates bounced up on Nov. 22, but a shipbroker quoted in a Reuters report expects dry bulk spot rates to stabilize in November and December “before a seasonally soft first quarter of 2022.” That would be some good […]

Wheat Exporting Countries Control Just 18% of Global Stocks

By Michael Anderson, USW Market Analyst As the U.S. wheat 2021/22 marketing year reaches its halfway point, U.S. Wheat Associates (USW) summarizes market factors affecting global wheat supply and demand with its farmer board of directors. The data comes from USDA’s October reports, which will be updated on November 9. We want to share some […]

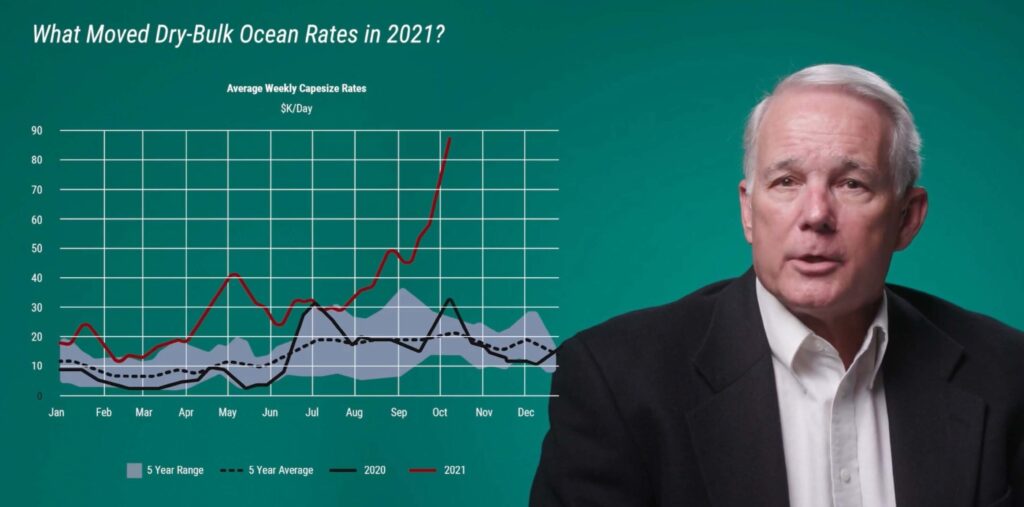

Freight Markets Ride the Waves of Uncertainty

Look at a line graph that tracks freight markets over the last two years and you may mistake it for the very waves the vessels traverse on the open ocean. Up and down the vessel goes, and so have the rates. The Baltic Dry Index (BDI), an assessment of the average cost to ship raw […]

Higher U.S. and World Wheat Prices Recall Another Bull Market

A surprising drop in USDA’s estimate of U.S. wheat production in the September 30 Small Grains Summary Report helped support the trend of higher U.S. and world wheat prices. The recent sustained run-up in prices calls to mind another (and even more challenging) bull wheat market beginning in marketing year 2006/07 and continuing through 2007/08. […]

How to Understand and Utilize the U.S. Wheat Associates Price Report

The U.S. farm families who produce wheat and the entire U.S. supply chain remain committed to operating a transparent and open market. How export prices are discovered is one of the reasons why our overseas customers know they can depend on the integrity of our supply chain, the quality of U.S. wheat and our unmatched […]

USDA’s Latest Look at Exportable Wheat Supplies

On Tuesday, Sept. 14, 2021, U.S wheat futures gained as much as 2% after key wheat-producing nations lowered their production outlooks. With harvest nearly wrapped up in the Northern Hemisphere, the most recent USDA Supply & Demand (WASDE) report brought an updated look at key exporting countries and regions. USDA currently expects 2021/22 world exportable […]

Farm Progress Survey Points to More Wheat, Corn, Soybean Acres

An August 2021 survey of 737 farmers across the United States conducted in late July by Farm Progress Publications suggests that wheat, corn and soybean planted area will be up for 2022. Jacqueline Holland, writing in www.farmprogress.com, said the surveyed farmers estimated they will plant a total of 46.7 million acres of wheat. Farm Progress […]

Global Wheat Stocks-to-Use Ratio Supports Bullish Prices Outlook

USDA’s August 2021 World Supply & Demand Estimates (WASDE) report trimmed expected global wheat production, reduced the global wheat stocks-to-use ratio and created a supply shock market rally. USDA dropped total production to 777 million metric tons (MMT), 15.4 MMT less than its July forecast, citing major weather problems in Russia, Canada and the United […]

Checking the 2021/22 Global Wheat Crop Ahead of August WASDE Report

The effects of weather on the 2021/22 global wheat crop have sparked a run-up in prices even as harvest progresses in the Northern Hemisphere. Given the market’s supply concerns, U.S. Wheat Associates (USW) gathered information from major wheat exporting countries to see what may affect USDA’s next estimates of world supply and demand due on […]

Agriculture Calls on STB to Increase Rail Competition Following Executive Order

On the heels of a White House Executive Order on competition this month, a large group of agricultural shippers recently wrote to the U.S. Surface Transportation Board (STB) to advocate for several policy proposals in front of the board that can make a significant difference in increasing rail competition in transportation of wheat and other […]